April 16, 2015

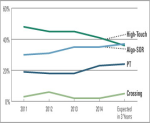

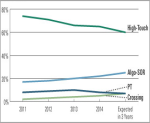

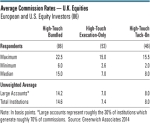

Our recent report, “Equity Trade Commissions: Rates Vary Broadly Across and Within Markets,” highlighted an interesting finding from a Greenwich Associates study: average bundled commission rates on equity trades are surprisingly consistent...

Categories:

Equities, Market Structure

Free Tags:

Bundled, commission, Execution-only, High Touch, rates, Tack-on