Complex regulations in both interest-rate derivatives and U.S. Treasuries are constraining profits for brokers and creating new buy-side demands.

The top five’s share of both product sets averages around 55% and Greenwich Associates expects the rates-trading business to concentrate even further into the hands of a small number of “flow monsters.” But with 45% of the market still up for grabs, mid-tier global dealers, regional dealers and alternative liquidity providers will fight tooth-and-nail for every last percent.

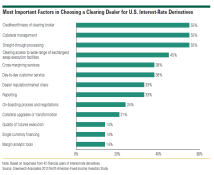

Methodology

Between February and April 2014, Greenwich Associates interviewed 1,067 U.S. institutional investors active in fixed income.

Interview topics included trading and research activities and preferences, product and dealer use, service provider evaluations, market trend analysis, and investor compensation.